Welcome to San Diego Blog | February 15, 2018

Real Estate vs. Stocks: Which Has Performed Better Over 145 Years?

What’s a better investment, stocks or real estate? And, while we’re asking this grandiose question, what’s a safer investment?

You probably have an opinion already as to the answer to both of these questions. It’s good to have opinions about important questions. And these certainly are important questions – they directly affect how you grow your wealth.

But opinions are never as useful as facts.

A team of economists from the University of California, Davis, the University of Bonn, and the German central bank, set out to answer these questions by analyzing a stunning amount of data.

Answer it they did. Ready for 145 years of economic data, summarized over the next five minutes for you?

The Rate of Return on Everything

The lead authors of the study – Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor – reported the findings of their massive study in a paper entitled The Rate of Return on Everything, 1870-2015. In it, researchers looked at 16 advanced economies over the past 145 years. Specifically, they compared returns on equities, residential real estate, short-term treasury bills, and longer-term treasury bonds.

With each asset type, they adjusted for inflation and included all returns, not just appreciation. Dividend income was included for equities, and rental income was included for residential real estate.

Their findings, in short: Residential real estate had the best returns, averaging over 7 percent per annum. Equities weren’t far behind, at just under 7 percent.

Then came bonds and bills, with far lower returns (surprising to no one).

Related: Worried About a Stock Market Crash? Prepare for the Bear Without Fear

Equities vs. Real Estate

Rental income proved an important factor – roughly half of the returns on real estate came from rents, while the other half came from appreciation.

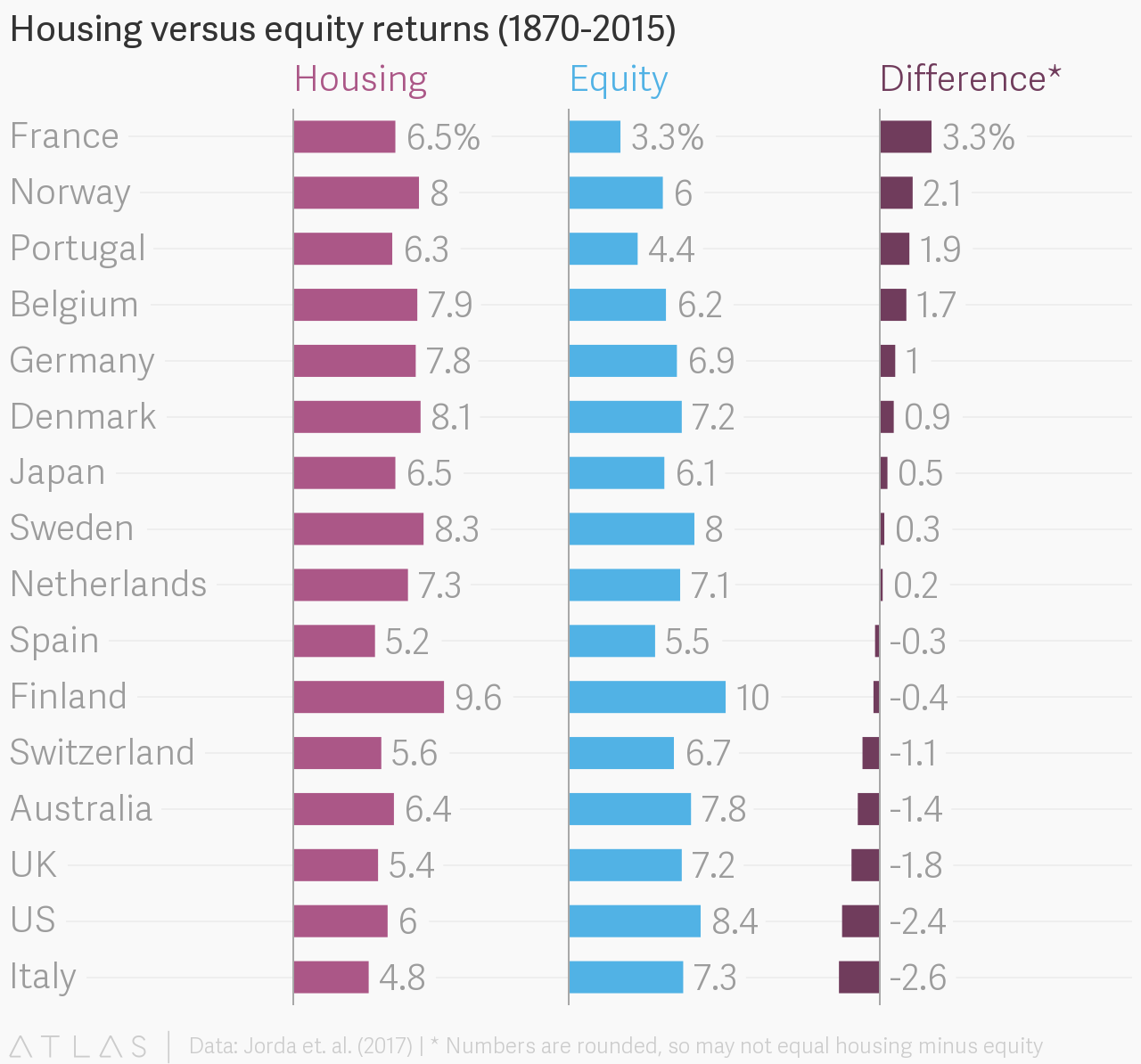

Equities and real estate each performed differently in various countries, of course. Here’s a comparison of each of the 16 countries when considering equities versus real estate:

Keep in mind, these are long-term averages over the course of many decades. In real time, these returns bounced up, down, sideways, and in circles.

Here’s a curious little chestnut for you: from 1980-2015, equities have, on average, performed significantly better than real estate. Across the 16 countries studied, equities earned an average annual return of 10.7 percent, decisively beating real estate’s stolid 6.4 percent.

Should we all sell our rentals and buy stocks?

Of course not. But the reasons are multiple and a bit nuanced.

First, a few outlier countries threw off the average returns from 1980-2015. Japan saw its real estate markets collapse as its population aged and started declining. In Germany, real estate has been stuck in the slow lane for decades.

Meanwhile, equities in Scandinavia have exploded.

But the most interesting case for real estate lies in its risk-reward ratio.

Of Risk and Volatility

Let’s do a quick stereotype check-in, shall we?

Treasury bonds are low-risk, low-return. I don’t think anyone’s prepared to challenge that stereotype – after all, stereotypes exist for a reason, right?

Equities are high risk, high return. This one gets a little more interesting, but a quick look at how stock markets have gyrated for the last century – up 29 percent one year and down 18 percent the next – should disabuse anyone of the notion that equities don’t come with high volatility and risk.

And that brings us to an economic assumption that dates back to, well, the beginning of economic theory. Economists have long held as a given that risk and returns are highly correlated, and that “the invisible hand” of the market will ensure that remains the case.

Why? Because if an asset were low-risk, high-return, everyone and their mother would fling so much money at it that the returns would dry up faster than Lindsay Lohan’s acting career.

Except that assumption hasn’t held true for residential rental properties.

Rental Properties: Low Risk, High Returns

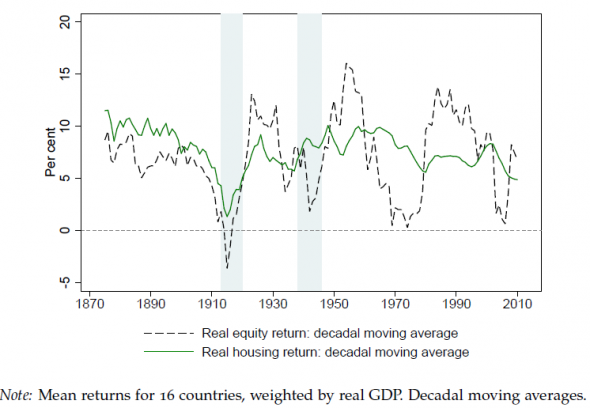

Throughout modern history, residential real estate has actually boasted extremely high returns with low risk. Take a look at volatility for equities versus real estate for the past 145 years:

Brighter economics minds than mine are scratching their heads as to why that is. But since I can’t resist offering a (you guessed it!) opinion, here are a few thoughts as to why.

First, real estate is expensive. Until the past ten years, with the advent of crowdfunding, you couldn’t invest your extra $100 a month in it like you could do with stocks.

Even if you leverage to the hilt and borrow the maximum mortgage allowed, that still usually puts you at 20 percent down, plus thousands of dollars in closing costs. Which says nothing of credit requirements, income requirements, and/or lenders’ requirements for investing experience.

In other words, real estate investing has a high barrier to entry.

It’s also difficult to diversify for those very same reasons. If each asset requires $20,000 in cash to purchase it, then it takes a lot of money to build a broad, diverse portfolio.

Real estate is also notoriously illiquid. You can’t buy it and sell it on a whim – it typically takes months to do either one.

But hey, that’s also precisely why it’s so much more stable than equities.

Related: The Irrefutable Advantage Real Estate Investors Have Over Stock Investors

Sharpe Ratios & Measuring Risk vs. Return

How do you measure an investment’s risk against its return?

It turns out, there’s a simple way to do this, a literal risk-reward ratio. It’s called the Sharpe ratio after its creator, William Sharpe.

You start with an asset’s return, and subtract out the return of the going with a short-term, risk-free alternative (like U.S. Treasury bills). That gives you a “risk premium” – the extra return the asset delivers, over a risk-free investment.

Then you simply divide that “risk premium” over the asset’s volatility, as measured by its annual standard deviation in value:

Risk Premium

___________________________

Average Annual Standard Deviation

If the math is giving you a headache, don’t worry about it. Just think of it as return divided by risk. A higher ratio indicates a better investment – greater return, relative to the risk.

Treasury bonds clocked in at a Sharpe ratio of around .2. Weak sauce.

Equities weren’t much better, at .27. Sure, their returns were strong, but they’re more volatile than plutonium in a mad scientist’s lab.

But residential real estate? It averaged a Sharpe ratio of .7.

For everyone who didn’t like the look of how real estate returns have compared to stock returns over the past few decades, consider that the Sharpe ratio for real estate has only grown stronger over time. Since 1950, the Sharp ratio for real estate has averaged an impressive .8.

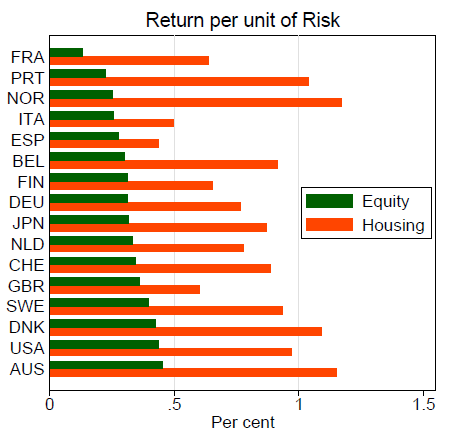

Another way of looking at it is return per unit of risk – here’s how equities have compared to real estate in each of the 16 countries studied:

Returns & GDP

Advanced economies tend to have slow economic growth, right? So how have returns done so much better than the GDP growth in these countries? Aside from the obvious issue that these economies looked very different in 1870 than they do today, there’s an interesting answer to this query.

It turns out, a country’s returns on its equities and real estate are not tied in a 1:1 relationship with its GDP. Over time, returns on these assets tend to average growth around double the speed of the country’s economy as a whole – measured by GDP (see chart at right).

It turns out, a country’s returns on its equities and real estate are not tied in a 1:1 relationship with its GDP. Over time, returns on these assets tend to average growth around double the speed of the country’s economy as a whole – measured by GDP (see chart at right).

If anything, that “returns average double GDP growth” summary is skewed low, because it includes the weak returns on bonds and bills. On average, equities and real estate perform several times better than GDP growth.

This helps explain why income inequality tends to expand over time in advanced economies. The average Joe does not own stock, and if he owns any real estate, it’s his one individual home – a home that he probably only earns appreciation on with no rental income (and remember, rental income makes up half of real estate’s returns!).

So how does Average Joe’s finances improve? Only through a raise. His raise is tied to how his employer is doing, which, in turn, is tied to how the economy is doing.

In other words, Average Joe’s finances are tied to GDP growth.

But Wealth Wise Wendy, who’s not nearly so average as Joe, invests as much money as she can in equities and real estate. She builds a portfolio of passive income that earns money even while she sleeps. That income is based on the returns of her investments, not based on the economy.

Conservatives and liberals can argue all they want about how much to redistribute wealth. But as an individual, you want to be like Wendy, not Joe. You want your wealth and income tied to the returns of equities and real estate, not tied to GDP.

Where Do Bonds Fit in This Discussion?

Bonds are boring.

No, really. We already talked about how they’re low risk, low return. Why bother with them if you can invest in rental properties, which are low risk, high return?

A common opinion I hear people say is, “Bonds may not have performed well over the past 15 years, but that’s abnormal! Just look at how well they did in the ’80s!”

Interestingly, this new study disproves that notion. The high bond yields of the 1980s were actually the anomaly – in fact, if you look at bond returns over the past 145 years, there were many periods where they earned negative returns.

Want a few reasons why rental properties are better investments than bonds?

Here’s a simple one: bonds expire. They pay out for a specific term, then they stop paying. Rental properties keep paying forever.

And not only do they keep paying indefinitely, they pay more over time. With every year that goes by, fixed bond payments become less valuable in real purchasing power due to inflation. But rents rise right alongside inflation.

It’s actually your fixed mortgage payment that goes down over time in inflation-adjusted dollars! Then one day that mortgage payment disappears, and your rental cash flow explodes.

OK; yes, government bonds offer stability. They pay the same amount every month. They never call you about a leaky roof or stop sending payments because they spent too much on cigarettes and Bud Light that month.

But at what cost in returns?

If retirement looms on the horizon for you, familiarize yourself with sequence risk and how rentals affect the 4 percent rule so you don’t necessarily have to resort to bonds.

Should I Stop Investing in Equities and Just Buy Rental Properties?

Stocks may be a roller coaster, but in the long run, the good times outweigh the bad.

They also balance rental properties well. And as we discussed last week, when equities go down, residential real estate almost always goes up.

Equities are liquid. You can buy and sell at a moment’s notice. Real estate isn’t quite so easy to get in and out of.

Equities also offer truly passive income. I love talking about passive income from rental properties – I teach an entire course about it! But ultimately, rental income can never be as passive as dividend income.

It’s much easier to diversify with stocks as well. You can spread $500 across thousands of companies, in every region of the world, in every industry, at every market cap. You’d be lucky to get away with only putting down $5,000 on a single rental property!

Residential rental properties offer excellent returns with low volatility. I love rental properties. But that doesn’t mean there’s no place for equities in your portfolio.

If you invest well, rental income will start performing for you immediately. Equities will take longer; the stocks you buy today won’t produce significant income for you until 10, 20, 30 years from now. But they’ll grow in value for you at prodigious rates.

Build a portfolio of passive income from rentals and dividends, and when your peers are still working in a decade or two, their incomes tied to GDP growth, you can offer sympathetic words.

And then you can go back to playing golf and relaxing with your children, having reached financial independence.

What are your thoughts on stocks versus residential real estate? Do you disagree with my dismissive attitude towards bonds? How do you decide how to allocate your assets and investments?

Bring on the opinions in the comments below!

Source: Bigger Pockets

Written by: admin

Categories: Buyers, Finance, Property Management, Property Management, Real Estate Investment, Real Estate Tips for Buyers, San Diego Condos, San Diego Real Estate, Tips for Buyers, Uncategorized