Welcome to San Diego Blog | May 20, 2021

Is a Real Estate Market Crash Coming?

No Crash Coming

Housing data illustrates that there is not a housing crash on the horizon.

Home prices were surging from 2000 through 2006. Homeowners were sitting back in their recliners watching their home value skyrocket to the heavens. It seemed like the housing market was unstoppable. Then it all came tumbling down with the beginning of the subprime meltdown in March 2007. Values dropped like a rock. Many lost their homes to foreclosure or short sale. Everybody remembers the scars of the Great Recession. Either they were directly affected, or it happened to somebody they knew.

Once again, housing is soaring upward with seemingly no end in sight. Buyers are tripping over each other, willing to pay tens of thousands of dollars above the asking price. Throw in the news of rising inflation and the potential of drastically higher mortgage rates, the madness must come to a screeching halt soon, right? Even though so many are anticipating and reporting that a housing crash is imminent, it simply is not going to occur, not now, not in the next 6-months, and not in the foreseeable future.

The Great Recession was triggered by the housing market where anyone could purchase a home regardless of their true qualifications. Zero down payment loans, negative ARM’s, cash out refinancing, subprime lending, and fudged loan documents all contributed to the astonishing rise in values that inflated the housing bubble that ultimately collapsed in 2007. The housing market crashed, and home values plunged.

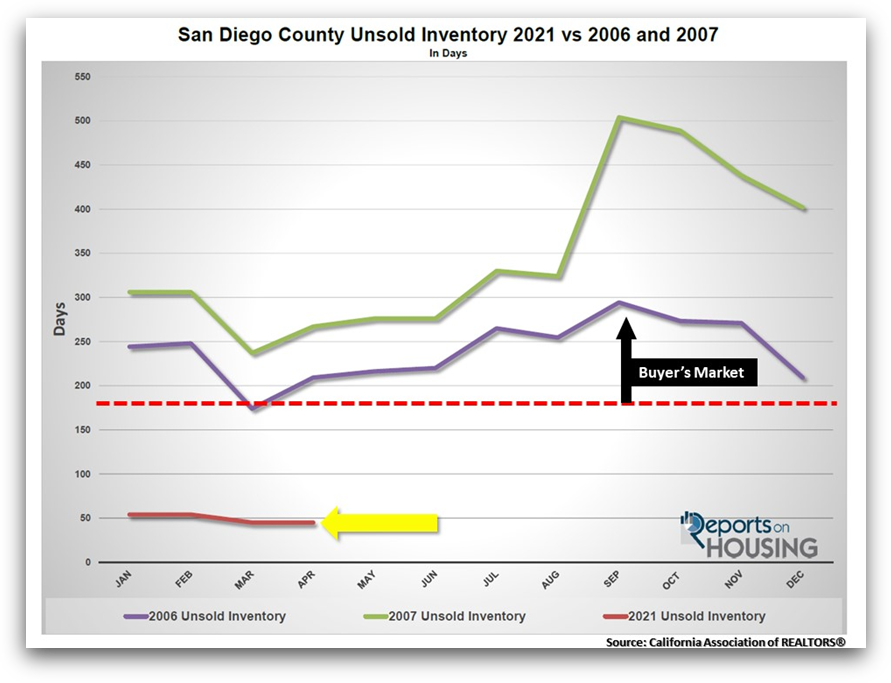

What occurred can be explained by looking at supply and demand. When supply rises and demand drops, the unsold inventory climbs. When supply drops and demand rises, the unsold inventory falls. The writing was already on the wall a couple of years prior to the start of the Great Recession. Housing data illustrated market conditions that were lining up in favor of buyers. The inventory swelled while demand crumbled. As a result, the unsold inventory rose to unfathomable heights. In April 2006, it surpassed 180 days, a Buyer’s Market. It grew to 294 days by September. In 2007, it surpassed 300 days in July, the start of the subprime meltdown. In September, it eclipsed 500 days.

Contrast that to today and the landscape is entirely different. The inventory is at unprecedented record low levels and demand, fueled by historically low rates below 3%, is off the charts. April’s unsold inventory in Los Angeles County hit 45 days, an extremely crazy, nutty, Hot Seller’s Market, where home values are surging higher every month, sellers get to call the shots, and most home sales are closing well above their asking prices. It will remain a Hot Seller’s Market for the remainder of the year based on the anemic inventory and today’s crazy demand.

The big difference is supply and demand. Currently, the active listing inventory is at 3,432 homes. Back in October 2006, there were over 15,000 homes. In 2007, there were over 18,000 homes, over seven times today’s supply. The current demand (the last 30 days of new escrows) is at 3,432. In 2006 and 2007 demand remained below 2,000 pending sales. With an enormous supply and weak demand, unsold inventory reached very high levels prior to the Great Recession, a precursor to the massive slide in home values.

There are some naysayers who are calling for a massive spike in mortgage rates due to inflation. Last week’s Consumer Price Index appeared to be soaring out of control with a 4.2% increase over last year. Yet, in taking a closer look at the numbers, the Federal Reserve is correct in their anticipation of “transitory,” or short-lived, inflation. The rise had more to do with short-term supply chain problems in lumber and a global chip shortage. Used cars jumped 10% as car rental companies clamored to restock their depleted inventories. Sporting event prices surged 10.1%, airline tickets climbed 10.2%, and hotel rooms were up by 8.8%. These were all discounted prior because of the pandemic. All other goods were unchanged. As a result, mortgage rates have not moved and remain just below 3%.

Mortgage rates are forecasted to rise to about 3.5% by year’s end due to an improving economy that is emerging from the pandemic. The rise will not dismantle the housing market; instead, it will decelerate the market from an insanely Hot Seller’s Market with the unsold inventory of 45 days to a regular Hot Seller’s Market with a market time above 90 days.

The Bottom Line: The housing market is NOT going to crash. The inventory is low, demand is high, market time is at all-time lows, mortgage rates are at record low levels, buyers must qualify for mortgages, subprime, and zero-down loans are not fueling housing, and homeowners have plenty of equity.

Copyright 2019 – Steven Thomas, Reports On Housing – All Rights Reserved.

Written by: Dannecker Team

Categories: Uncategorized