Welcome to San Diego Blog | January 27, 2022

San Diego County Housing Report: Rising Rates Vs. No Inventory

There are two opposing economic forces impacting the

housing market right now, rising mortgage rates, and a record

low supply of homes available to purchase.

Opposing Forces

There simply are not enough homes available for buyers and rising rates have not yet had an impact on the insanely hot housing market.

The supply chain problems have been well documented across the United States and around the globe. One of the hardest-hit industries is new cars. The supply of available new cars has dwindled down to record lows. As a result, dealers are adding a “market adjustment fee,” a line-item cost above the MSRP. The fee ads anywhere from a few thousand dollars to as much as $20,000 more for a popular model. It has everything to do with supply and demand. Consumers looking for a new car are confronted with very few options and rising car prices. To get their hands on one, many are willing to pay the surcharge.

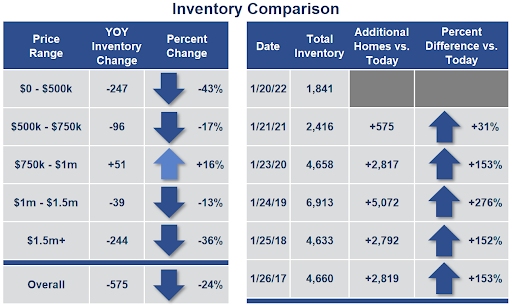

Housing feels like it too is suffering from the supply chain problem with seemingly nothing available to purchase. Last year the inventory in San Diego County started the year at an all-time low with 2,556 available homes. It hit 2,175 on April 1st, rose and peaked in August, and then continued to plunge until only 1,254 homes were on the market on January 1st of this year, just a few weeks ago. Today, there are 1,841 homes, adding 587 during the first few weeks of the year. The difference between this year’s and last year’s record low is striking. There are 575 fewer homes today, 24% less. Every price range has been impacted except for homes between $750,000 and $1 million, where there are 16% more than last year.

Comparing today to every year since 2017 is mind-blowing. In 2019, prior to the pandemic, there were 5,072 additional homes on the market, 276% more, three-and-a-half times the number of homes today. In 2017, 2018, and 2020, there were around 2,800 additional homes on the market in each of those years, about 153% extra, two-and-a-half times more than today. Comparing today’s level to prior years illustrates just how acute today’s inventory crisis has become.

The inventory was already trending lower prior to the pandemic, but the pandemic accelerated the issue as fewer homes were placed on the market despite soaring demand. In 2020 and 2021 combined, there were 12,800 fewer FOR-SALE signs compared to the average number between 2017 and 2019, 12% less.

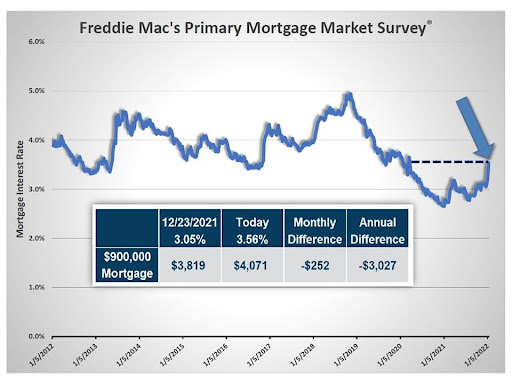

Since ringing in a New Year, mortgage rates have been steadily climbing, eroding home affordability. According to Freddie Mac’s Primary Mortgage Market Survey®, rates have risen from 3.05% on December 23rd to 3.56% as of January 20th, up a half of a percent in just 4-weeks. It has many speculating that even higher rates are coming. Throw in a volatile stock market, and many are beginning to wonder if these changes are just the beginning of the end to the pandemic run on the housing market.

First, it is best to explain why mortgage rates have been moving higher. Investors and Wall Street had already digested the fact that the Federal Reserve was tapering their purchases of Mortgage-Backed Securities and were going to be raising the Short-Term Federal Funds Rate (tied to automobile loans and credit card debt and NOT to 30-year mortgages) starting this March. Additionally, they just announced that they were going to be draining their balance sheets. That was unexpected. The Federal Reserve went from calling inflation transitory, or temporary, and doing nothing just a few months ago, to acknowledging that it was an issue and that they were going to do everything in their power to slow inflation’s grip on the economy. It was as if the Fed acknowledged that they made a mistake and that they were behind the 8-ball, and now they are engaging in a “hurry-up offense” style to try and make up for the lost time. The markets reacted and rates rose by half a percent in 4-weeks.

There is an impact on rising rates. The rise from 3.05% to 3.56% is an additional $252 per month for a $900,000 mortgage, or $3,027 per year. However, with such a limited supply of available homes, the impact is not being felt on the street. Today’s rate may be the highest since the start of the pandemic, but it is still a really great rate. The extra $252 per month is more of a “market adjustment fee” for housing that is easily absorbed due to the extremely limited number of homes available. Homes are still flying off the market as fast as they are coming on. Throngs of buyers are waiting in lines for the opportunity to see a home that is placed on the market. Multiple offers are the norm. After receiving 10, 20, or 30 offers on a home, the sellers are calling all the shots, sales prices exceed their asking prices, and home values continue to rapidly rise.

Why has the rise in rates not yet affected the housing market? The answer is simple: rates have not climbed high enough to materially slow demand. Mortgage rates climbed considerably in both 2013 and 2018, which caused a shift in the market. Demand cooled, the inventory increased, market times grew, and the market slowed from a Hot Seller’s Market to a much more balanced market. In 2013, rates rose from 3.34% to 4.57%, and in 2018 they rose from 3.99% to 4.94%. The recent runup in rates is much smaller. If they continue to climb, then the market could cool. But, for now, Wall Street and investors have digested future Federal Reserve moves and they most likely will not rise much more from here. Rates would need to climb to 4% or higher to slow housing. At 4%, the difference in payment for that same $900,000 mortgage example would be $478 more per month or $5,739 per year. At 4.25%, it would be $608 per month or $7,299 per year.

The recent rise four-week rise in mortgage rates had no real impact on the current pace of housing. It will be important to watch how mortgage rates unfold in the weeks and months to come. Until rates rise substantially from here, it is business as usual, an insanely hot housing market in San Diego County.

Copyright 2019 – Steven Thomas, Reports On Housing – All Rights Reserved. This report may not be reproduced in whole or part without express written permission by the author.

Written by: Mia

Categories: Market Conditions