Welcome to San Diego Blog | June 11, 2026

What Sticky Inflation Means for Your San Diego Move

Recent economic data shows inflation is remaining stubborn. But before the local headlines send you into a panic, let’s break down what is actually happening and what it means for buyers and sellers in San Diego County.

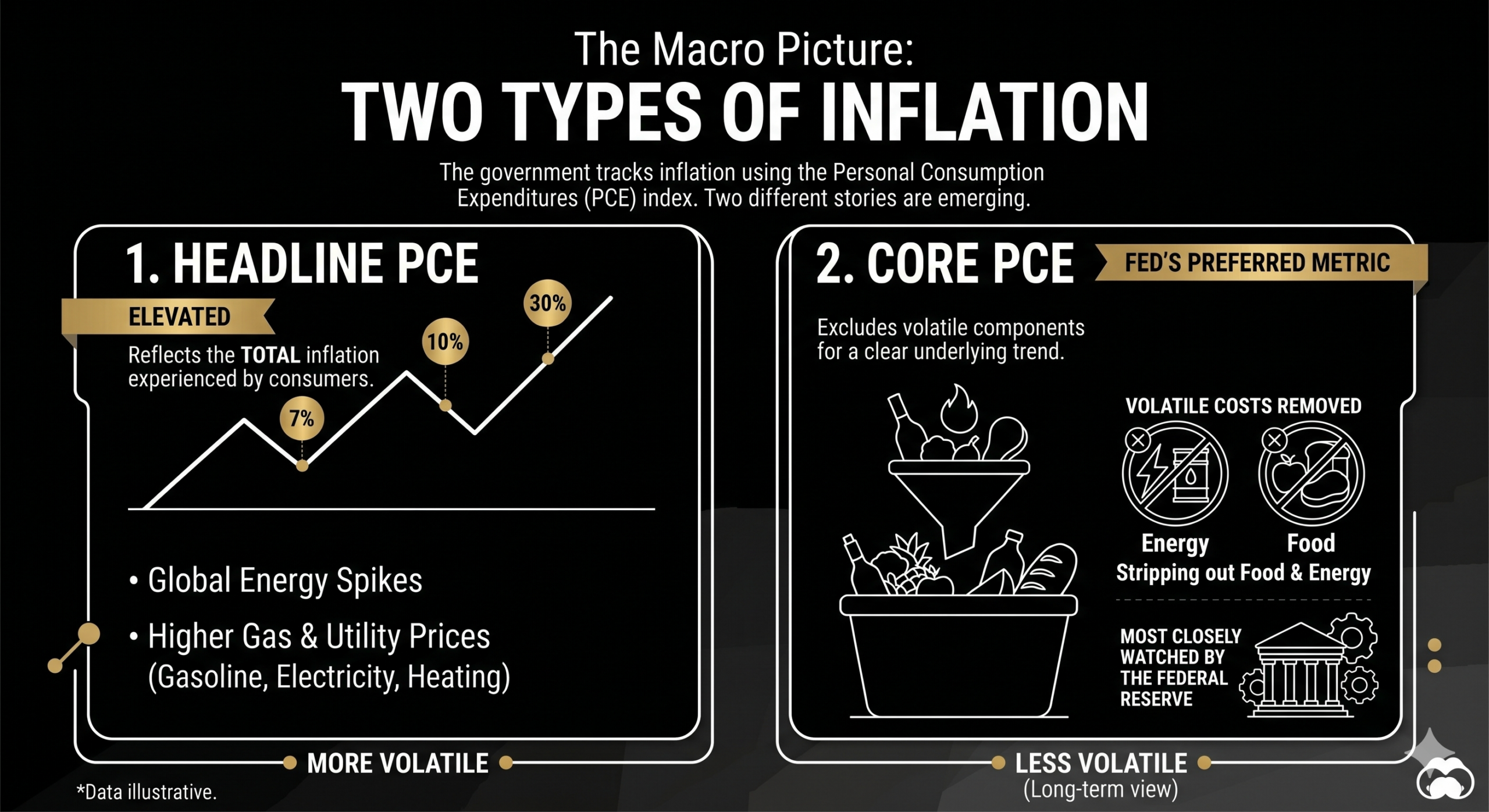

The Macro Picture: Two Types of Inflation

The government tracks inflation using the Personal Consumption Expenditures (PCE) index. Right now, we are looking at two different stories:

- Headline PCE: This number is elevated, largely because global energy spikes have driven gas and utility prices higher.

- Core PCE: This is the metric the Federal Reserve watches closest. It strips out volatile food and energy costs.

The Silver Lining: Core PCE is rising much slower than headline inflation. This indicates that once international energy pressures ease, overall inflation should follow.

The Impact on San Diego Mortgage Rates

Because inflation remains sticky, the Federal Reserve is keeping its benchmark interest rate elevated. While it is not a direct one-for-one link, this macro pressure keeps mortgage rates from dropping as fast as local buyers had hoped.

If you are waiting for rates to return to the 4% range before buying a home, you may be waiting a long time. Economists project that “higher for longer” is the reality for the foreseeable future.

Why a 2008-Style Crash Isn’t Coming

A tough economy does not equal a housing collapse. Today’s San Diego market rests on completely different fundamentals than the 2008 recession:

- Permanent Inventory Shortage: San Diego’s unique geography—bounded by the Pacific Ocean, mountains, and the Mexican border—creates a natural supply ceiling. We have a structural housing deficit, not a flood of oversupply.

- Historic Equity Protection: With the county’s median single-family home price hovering around $1,074,000, local homeowners are sitting on massive equity cushions.

- Strict Credit Standards: Unlike the mid-2000s, homeowners over the last decade faced rigorous lending qualifications. Today’s challenge is strictly an affordability squeeze, not a wave of foreclosures.

Tactical Moving Strategies for This Market

High rates simply mean your strategy needs to shift. Buyers and sellers are successfully navigating the county right now using a few specific tactics:

- Seller Concessions: Savvy buyers are successfully negotiating temporary 2-1 or permanent rate buydowns financed entirely by the seller to lower their initial monthly payments.

- Assumable Loans & ARMs: Certain FHA and VA loans allow qualified buyers to take over the seller’s original low rate. Adjustable-Rate Mortgages (ARMs) are also offering lower entry-level payments.

- Targeting Hidden Value: While coastal luxury remains highly competitive, strong relative value can still be found in expanding sub-markets like South Oceanside, East Chula Vista, Downtown San Diego or Mira Mesa.

Chad’s Perspective

Waiting for mortgage rates to drop before you buy a home in San Diego is a trap.Think about it: the exact minute interest rates drop significantly, every single buyer who has been sitting on the sidelines is going to storm the market at the same time. In a supply-starved city like ours, that sudden surge of demand will instantly trigger absolute chaos—bidding wars will return, and home prices will feel upward pressure. You might get a slightly lower interest rate, but you’ll end up paying an extra $50,000 to $200,000 for the exact same house.If you find a home you love and the monthly payment fits your budget with a strategic loan product today, buy it. You can always refinance when the economy eventually cools off. But remember: you can refinance a bad rate, but you can never refinance an overpaid purchase price from a future bidding war. Marry the neighborhood, date the rate, and play the long game.

For a deeper dive into how hyper-local market factors are shaping current real estate choices, check out this breakdown of what is happening in the San Diego real estate market right now. This video is highly relevant because it explores how local factors like neighborhood-specific pricing trends and changing insurance realities are impacting buying power across San Diego County today.

Written by: Dannecker Team

Categories: Market Conditions, Market Trends, San Diego Real Estate